…that depends on who you ask

Since real GDP (Gross Domestic Product) fell for the first two quarters of 2022, many in the media, the financial press, and politicians have concluded that the U. S. is in recession, stirring up a lot of debate and even controversy. This conclusion is based on the Rule of Thumb that two consecutive quarterly drops in real GDP constitutes a recession. This is called the 2 Quarter (2Q) rule. Please note that a rule of thumb is not a scientific law. Merriam-Webster dictionary defines rule of thumb as “a general principle regarded as roughly correct but not intended to be scientifically accurate.”

In 2011, I and a colleague (Dr. Marjorie Fox) published a paper in the International Journal of Business and Economics Perspectives entitled, “Is it a recession yet? The answer depends on who you ask”.

One of the main conclusions we came to was that “… the 2Q rule provides neither necessary nor sufficient conditions for pinpointing the start of a recession.”1 In other words, sometimes falling real GDP for two consecutive quarters does not indicate the beginning of a recession while sometimes a recession may begin without the GDP falling two quarters in a row. In the second and third quarters of 1947 real GDP fell by .6% and .3% respectively. Yet according to hindsight conclusions, no recession occurred. On the other hand, after GDP peaked in March of 2001, real GDP did not fall the next two quarters but the economy was deemed to have fallen into recession by the second quarter. Who determines when a recession begins and ends? Surprisingly it is not the government.

The Business Cycle Dating Committee of the National Bureau of Economic Research (NBER), a private research organization, is the entity that determines when a recession officially begins and ends. The Department of Commerce and other government entities accept their announcements as official. How does the NBER define a recession?

The NBER’s Business Cycle Dating Committee defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. A recession begins just after the economy reaches a peak of activity and ends as the economy reaches its trough. Between trough and peak, the economy is in an expansion. Expansion is the normal state of the economy; most recessions are brief and they have been rare in recent decades.”2 [Writer’s italics]. In short, the Business Cycle Dating Committee takes into account not just changes in real GDP but also changes in real income, employment, industrial production and wholesale-retail sales. If all of the aforementioned macroeconomic variables are falling over the two quarter decline in real GDP, the Committee would most likely deem the 2-quarter decline in real GDP to indicate a recession, as long as the overall decline is significant.

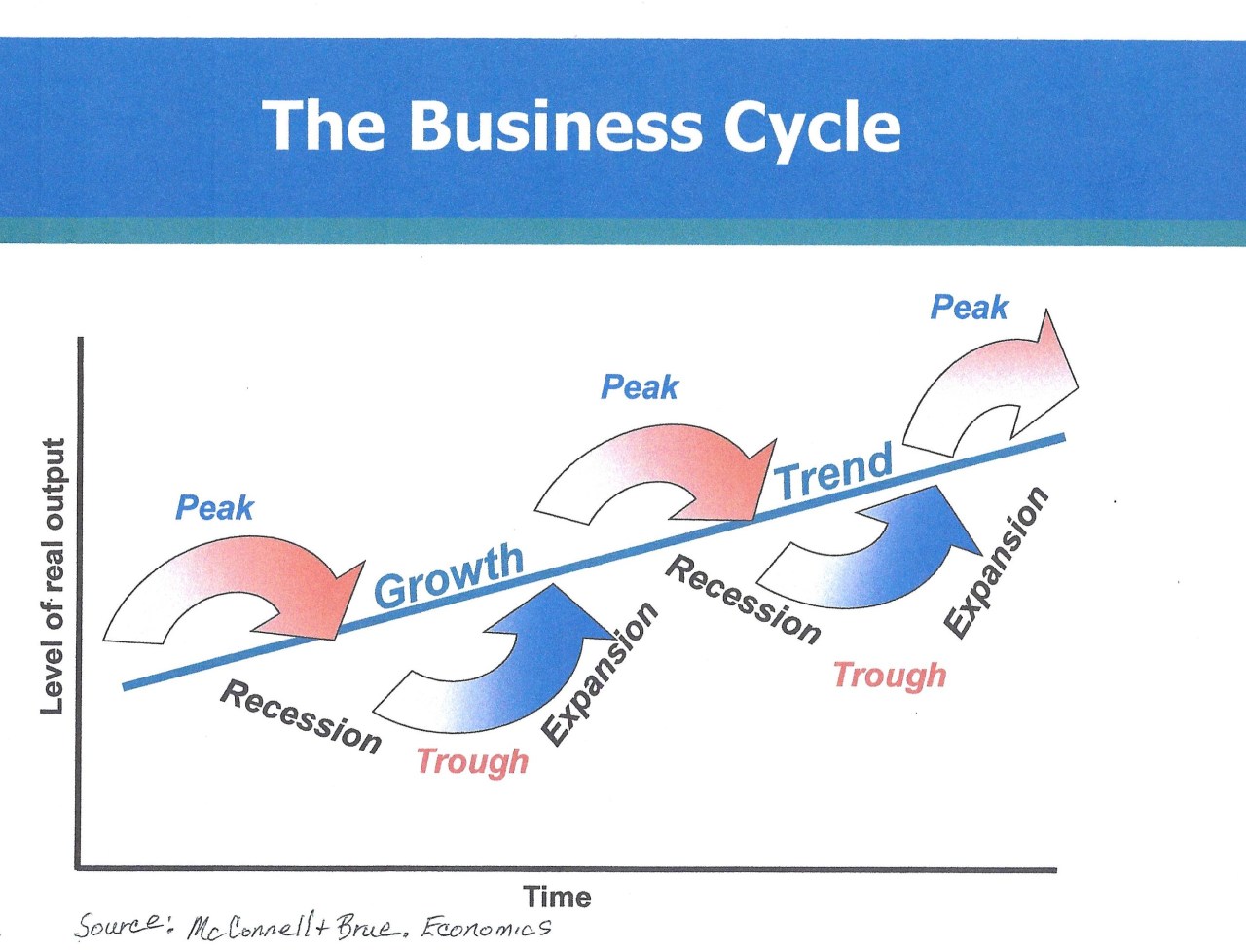

The preliminary estimates show that real GDP declined 1.6% and .9% in the first and second quarters of this year. These are not big numbers. Are they large enough to label the declines significant? We don’t know yet. When the estimates are revised, the final changes could go up or down. In terms of the featured graphic at the top of this post, are we in the pink recessionary phase of the Business Cycle or are we still hovering around the peak? Meanwhile employment is expanding. Is it a recession yet? My judgment is we don’t know but probably not.

Watch the Fed (the Federal Reserve). They are a good barometer. If the Fed thinks the economy is headed for recession or is in recession, they will be less aggressive in pushing up interest rates.

- Fox, Marjorie and Frank Martin (2011). International Journal of Business and Economics Perspectives Volume 6, Number 1, Winter 2011

- Retrieved from Business Cycle Dating Committee Announcement January 7, 2008 | NBER on July 30, 2020